Nigeria’s External Debt Rise Slower Under Tinubu Than Buhari, Data Shows; Currency Revaluation Drives Headline Increase

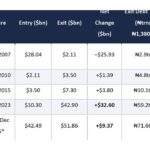

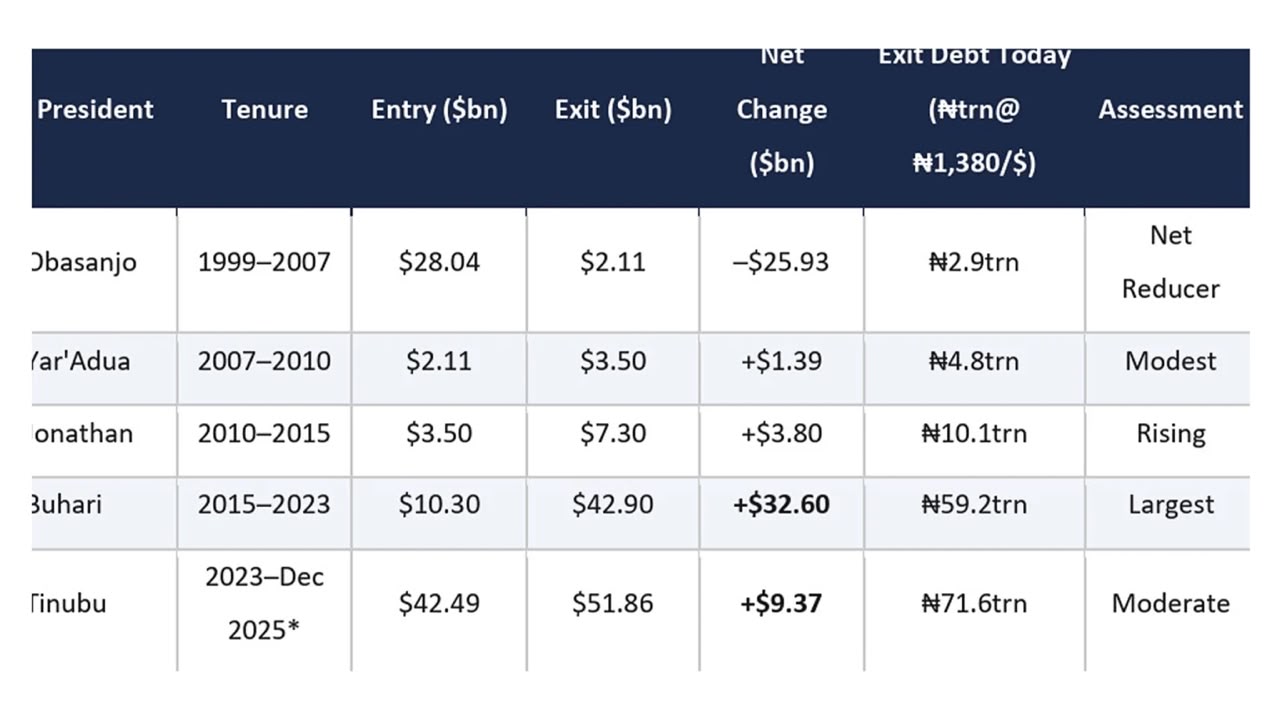

Nigeria’s External Debt Rise Slower Under Tinubu Than Buhari, Data Shows; Currency Revaluation Drives Headline Increase Recent data on Nigeria’s debt profile indicates that the country’s external debt has risen at a slower pace under President Bola Ahmed Tinubu than during the administration of former President Muhammadu Buhari, with analysts attributing much of the recent surge in naira terms to currency depreciation and statistical revaluation rather than fresh borrowing. According to data compiled in Nigeria’s long-term debt records covering 1999 to 2025, the apparent sharp increase in external debt in naira terms since 2023 is largely driven by exchange rate adjustments following reforms in the foreign exchange market.Between Q1 2023 and Q2 2023, external debt in naira terms rose from about ₦19.6 trillion under the end of the Buhari administration to roughly ₦33.2 trillion under Tinubu. However, this jump reflects revaluation effects caused by naira depreciation rather than a proportional increase in dollar-denominated borrowing. In dollar terms, Nigeria’s external debt stock has moved more gradually, with increases reflecting a combination of new borrowing, Eurobond issuances, and project financing rather than abrupt expansion. Data show external debt rising to about $51.86 billion by December 2025 from $42.49 billion in late 2023. Analysts say this divergence between naira and dollar figures highlights the impact of exchange rate unification and currency adjustments implemented under the Tinubu administration, which significantly altered the local currency valuation of existing foreign obligations. Under Buhari 2015–2023, external debt expansion was more closely associated with sustained borrowing over time, including multilateral loans and Eurobond issuances, which steadily increased Nigeria’s dollar-denominated obligations. In contrast, early data from the Tinubu era 2023–2025 suggest a more mixed picture: while new borrowing has continued, a significant portion of the headline debt increase is linked to revaluation effects and the restructuring of previously accumulated obligations, including fiscal adjustments and balance sheet clean-ups. Experts note that the country’s total public debt trajectory must be assessed using both currency-adjusted and dollar-based measures to avoid misinterpretation of fiscal trends, particularly in periods of major exchange rate volatility. Broader economic reports also show that Nigeria’s debt profile has continued to evolve alongside fiscal reforms, including subsidy removal, tax restructuring, and efforts to improve revenue mobilisation.

While concerns persist about rising debt servicing costs and fiscal sustainability, officials argue that recent reforms are aimed at improving transparency and aligning official debt figures with market realities rather than masking underlying liabilities. Economists say the key distinction between the two administrations lies not only in borrowing levels but also in how currency valuation changes have reshaped the presentation of debt figures in national accounts.

The debate over Nigeria’s debt trajectory continues as policymakers balance infrastructure financing needs with concerns about long term fiscal sustainability and exchange rate stability.